Understanding The Growth Of The Inferior Vena Cava (IVC) Filter Market By 2035

Inferior Vena Cava (IVC) Filter Market Industry 2025–2035

This market research report explores the evolving landscape of the Inferior Vena Cava (IVC) Filter Market from 2025 to 2035. As a critical segment within the global medical device industry, IVC filters are pivotal in preventing life-threatening conditions such as pulmonary embolism (PE) by capturing blood clots before they reach the lungs. The report investigates the current state of the market and provides a forward-looking perspective on key trends, technological innovations, growth drivers, segmentation, and competitive dynamics. It aims to inform industry stakeholders, medical professionals, investors, and policymakers about the developments in the IVC filter space, focusing on providing practical insights to navigate this high-potential market effectively.

Market Overview and Projections for IVC Filters (2025–2035)

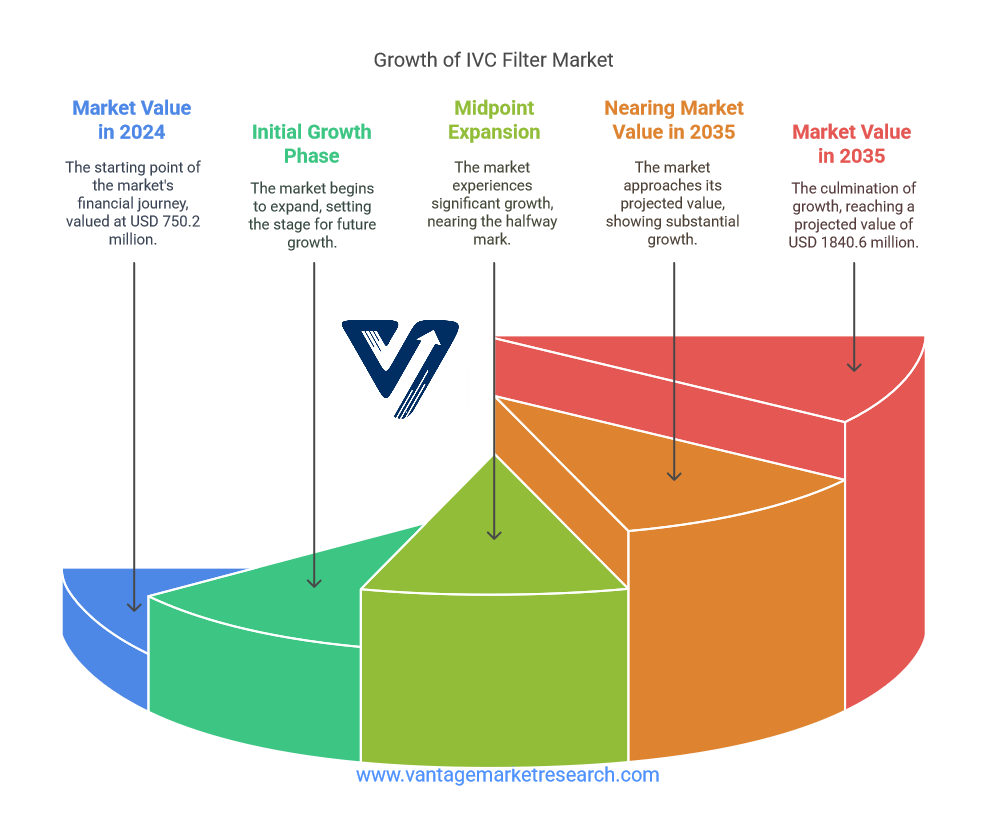

The Global Inferior Vena Cava (IVC) Filter Market has been undergoing significant transformation, reflecting broader changes in medical technologies and healthcare delivery systems. As of 2024, the market is estimated at approximately $750.2 million, with projections suggesting it will grow at a compound annual growth rate (CAGR) of 8.5% through 2035. This growth trajectory is underpinned by several converging factors: the rising global burden of venous thromboembolism (VTE), technological innovations in filter designs, increasing emphasis on preventive care, and a growing preference for minimally invasive procedures.

Download Sample Report PDF (Including Full TOC, Table & Figures) @ https://www.vantagemarketresearch.com/inferior-vena-cava-ivc-filter-market-4062/request-sample

Demographic trends such as aging populations in North America, Europe, and parts of Asia are particularly relevant, as older adults are more prone to conditions like DVT and PE. At the same time, sedentary lifestyles and chronic illnesses linked to obesity and cardiovascular risks continue to contribute to an expanding at-risk population. The COVID-19 pandemic also brought renewed focus on thrombotic complications, prompting healthcare systems to reevaluate and reinforce preventive strategies—an environment favorable to the IVC filter market.

Regulatory reforms and quality standards will also shape the future of the IVC filter market. Stricter guidelines from agencies such as the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA) influence product development cycles and post-market surveillance. Nonetheless, this regulatory environment encourages innovation and ensures that safer, more effective devices reach consumers.

Additionally, artificial intelligence and real-time imaging technologies are beginning to influence how IVC filters are deployed and monitored. Hospitals and surgical centers are increasingly integrating AI-assisted imaging tools for more accurate placements and fewer complications, improving patient outcomes and adoption rates. Over the next decade, these tools are expected to play an increasingly important role in the market's evolution.

Factors Driving Growth in the Inferior Vena Cava (IVC) Filter Market

One of the most prominent drivers of the IVC filter market is the rising prevalence of DVT and PE conditions worldwide. These life-threatening conditions affect millions annually and are exacerbated by both inherited and lifestyle factors. Prolonged immobility—whether due to hospitalization, long-haul travel, or sedentary occupations—continues to pose a serious health risk. Moreover, diseases such as cancer, stroke, and COVID-19 have been linked to increased rates of thromboembolism, further reinforcing the demand for preventive solutions like IVC filters.

Minimally invasive interventions have emerged as a cornerstone of modern medicine, replacing traditional open surgeries with techniques that reduce patient recovery times, minimize hospital stays, and lower complication rates. IVC filters—especially retrievable variants—align with this paradigm, offering physicians a less invasive method for managing thromboembolic risk in high-risk patients. Their ability to be removed once the patient’s risk diminishes provides flexibility and safety, encouraging greater adoption across diverse healthcare settings.

Another key driver is increasing patient and provider awareness. Health literacy campaigns, digital health platforms, and public health initiatives have all contributed to a greater understanding of VTE risks among patients and physicians. Medical professionals are now more proactive in identifying patients at elevated risk for PE and recommending preventive strategies such as IVC filters, particularly when anticoagulant therapy is contraindicated.

Technological advancements also play a crucial role. The product innovation pipeline is rich with next-generation solutions, from enhanced biocompatibility materials to smart filters capable of telemetry and remote diagnostics. These innovations are propelled by increased R&D investments, particularly in the United States, Germany, and Japan, where collaborations between academic institutions and private firms push boundaries.

Take Action Now: Secure Your Position in the Global Inferior Vena Cava (IVC) Filter Industry Today – Purchase Now.

Product Segmentation in the Inferior Vena Cava (IVC) Filter Market

Product segmentation in the IVC filter market primarily centers around permanent and retrievable filters, each serving distinct clinical purposes. Permanent IVC filters are implanted for long-term use in patients with a persistent risk of thromboembolism, such as those with chronic immobility or recurring clotting disorders. These devices offer durable protection but are associated with long-term risks like filter migration or perforation if not appropriately monitored.

Retrievable IVC filters, in contrast, are designed for temporary use. These are preferred in cases where thrombotic risk is expected to decrease, such as during a short-term postoperative period or transient contraindication to anticoagulation therapy. Their removability makes them attractive to physicians and patients alike, and over the last decade, retrievable filters have increasingly become the dominant product type.

Recent years have also seen the development of bioresorbable IVC filters, a major innovation in the field. These filters degrade naturally within the body after serving their purpose, reducing the need for retrieval procedures and lowering the risk of long-term complications. While still in the early stages of clinical adoption, bioresorbable filters are poised to transform the landscape by offering a blend of safety, efficacy, and convenience.

Further segmentation can be observed in terms of application settings—whether for emergency care, post-surgical recovery, oncology, or trauma management. Each of these verticals requires tailored filter solutions, which influence the market strategy of leading manufacturers.

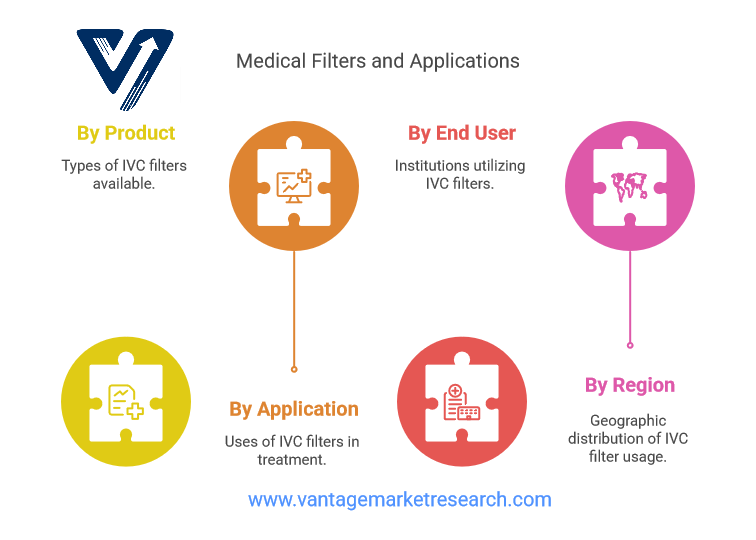

The global Inferior Vena Cava (IVC) Filter market can be categorized as Product, Application, End User, and Region.

By Product

- Retrievable IVC Filter

- Permanent IVC Filter

By Application

- Treatment of Venous Thromboembolism (VTE)

- Prevent Pulmonary Embolism (PE)

- Others

By End User

- Hospitals

- Ambulatory Surgical Centers (ASCs)

- Others

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

For the Inferior Vena Cava (IVC) Filter Market Research Report and updates, view the full report now!

Regional Insights and Competitive Landscape

North America remains the dominant global IVC filter market, accounting for more than 40% of the total market share. This is primarily due to its well-established healthcare infrastructure, favorable reimbursement policies, high patient awareness, and ongoing innovations from key industry players in the U.S. Rigorous FDA oversight has ensured high safety and performance standards, making North American products globally competitive.

Europe follows closely, driven by strong public healthcare systems, rising incidence of VTE-related conditions, and increased investments in diagnostic and therapeutic solutions. Countries such as Germany, the U.K., and France are at the forefront, though adoption in Eastern Europe remains uneven due to economic and infrastructural disparities.

Asia-Pacific, however, is emerging as the fastest-growing region for IVC filters. A rising middle-class population, greater healthcare access, and the increasing burden of cardiovascular diseases in countries like India and China fuel market expansion. In addition, government-led healthcare reforms and private sector investments are also enhancing the adoption of advanced medical devices across urban and rural settings.

In Latin America and the Middle East, the market is still nascent but growing steadily, with a rising focus on medical tourism and improved healthcare infrastructure acting as enablers.

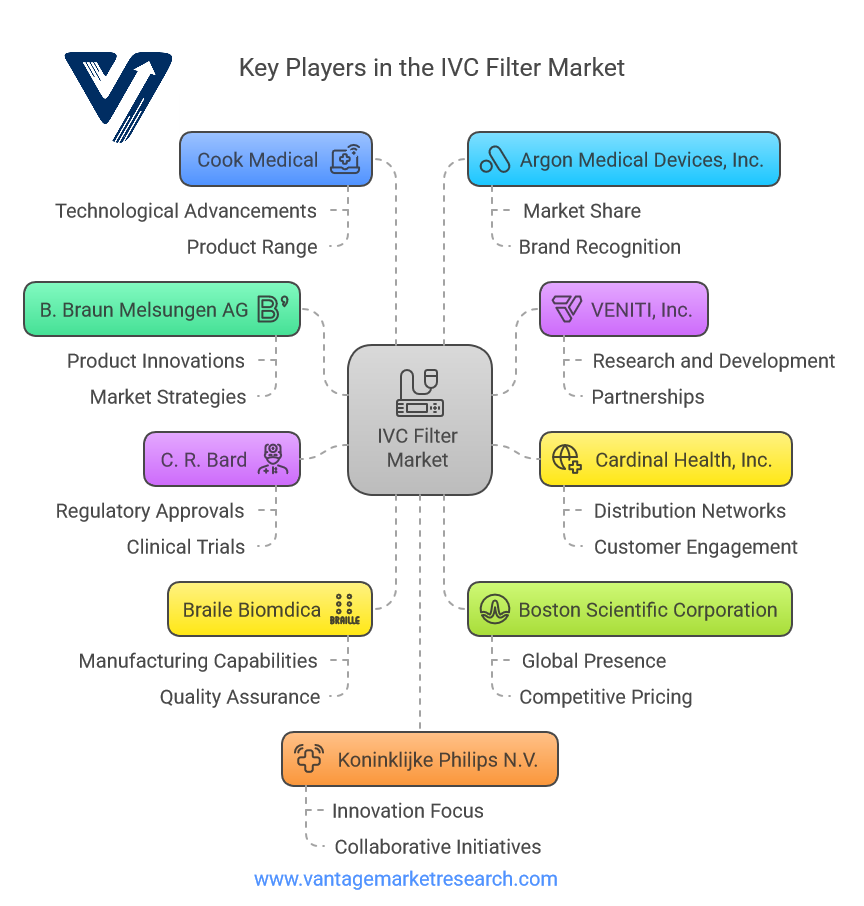

Top 10 Companies in Inferior Vena Cava (IVC) Filter Industry

- B. Braun Melsungen AG

- VENITI Inc.

- Cardinal Health Inc.

- C. R. Bard

- Braile Biomdica

- Boston Scientific Corporation

- Cook Medical

- Argon Medical Devices Inc.

- Koninklijke Philips N.V. (Philips Volcano)

- ALN

Key Players and Their Strategic Initiatives

The IVC filter market is moderately consolidated, with a handful of dominant players leading through innovation, strategic acquisitions, and strong distribution networks. Notable companies include:

- Boston Scientific Corporation: Known for its broad medical device portfolio, Boston Scientific continues to innovate in retrievable filter design and is investing in smart sensor integration for filter tracking.

- Cook Medical: One of the earliest entrants in the IVC filter space, Cook Medical remains a leader through product reliability and extensive physician education programs.

- C.R. Bard (now part of BD - Becton, Dickinson and Company): A pioneer in filter technology, Bard has launched numerous models and continues to refine its product line based on real-world usage data.

- Cardinal Health, ALN Implants, and Braun Melsungen AG also maintain significant market presence and are investing in next-generation product lines.

Key strategies among these players include mergers and acquisitions to broaden product portfolios, partnerships with hospitals and research institutions to validate clinical efficacy, and investments in emerging markets to capture new customer bases.

Conclusion

The inferior vena cava (IVC) Filter Market is on a robust growth path through 2035, driven by rising health concerns, demographic shifts, evolving surgical practices, and technological breakthroughs. Stakeholders across the value chain—manufacturers, providers, regulators, and patients—stand to benefit from this momentum, provided they stay attuned to the dynamic landscape. With continued innovation and strategic focus, IVC filters are set to remain a cornerstone of VTE prevention, marking their importance in the broader scope of global healthcare delivery.

FAQs

- What factors are driving the growth of the Inferior Vena Cava (IVC) Filter Market?

- How has the valuation of the global Inferior Vena Cava (IVC) Filter Market changed from 2024 to 2035?

- What is the projected Compound Annual Growth Rate (CAGR) for the Inferior Vena Cava (IVC) Filter Market?

- What are the key trends influencing the Inferior Vena Cava (IVC) Filter Market over the next decade?

- How does the CAGR of 8.5% impact the future of the Inferior Vena Cava (IVC) Filter Market?

- What are the key challenges facing the Inferior Vena Cava (IVC) Filter Market?

- How is the market for Inferior Vena Cava (IVC) Filters segmented?

Browse More Health Care Industry News

The global Weight Loss Drugs Market is valued at USD 2.88 Billion in 2024 and is projected to reach a value of USD 142.5 Billion by 2035 at a CAGR (Compound Annual Growth Rate) of 42.5% between 2025 and 2035.

The global Angina Pectoris Drugs Market is valued at USD 11.68 Billion in 2024 and is projected to reach a value of USD 18.56 Billion by 2035 at a CAGR (Compound Annual Growth Rate) of 4.3% between 2025 and 2035.

The global Photobiomodulation Market is valued at USD 249.5 Million in 2024 and is projected to reach a value of USD 514.5 Million by 2035 at a CAGR (Compound Annual Growth Rate) of 6.8% between 2025 and 2035.

The global Reproductive Hormones And Proteins Tests Market is valued at USD 4.2 Billion in 2024 and is projected to reach a value of USD 7.8 Billion by 2035 at a CAGR (Compound Annual Growth Rate) of 5.9% between 2025 and 2035.

Editor Details

-

Company:

- Vantage Market Research

-

Name:

- Rahul

- Email:

-

Telephone:

- +12129511369